Autocorrelation Function

Acf.RdPlot the ACF without the traditional noninformation unit spike at lag 0.

Usage

Acf(x, lag.max = NULL, type = c("correlation", "covariance", "partial"),

plot = TRUE, na.action = na.fail, demean = TRUE, ...)

# S3 method for class 'Acf'

plot(x, ci = 0.95, type = "h", xlab = "Lag", ylab = NULL, ylim = NULL,

main = NULL, ci.col = "blue", ci.type = c("white", "ma"),

max.mfrow = 6, ask = Npgs > 1 && dev.interactive(),

mar = if (nser > 2) c(3, 2, 2, 0.8) else par("mar"),

oma = if (nser > 2) c(1, 1.2, 1, 1) else par("oma"),

mgp = if (nser > 2) c(1.5, 0.6, 0) else par("mgp"),

xpd = par("xpd"), cex.main = if (nser > 2) 1 else par("cex.main"),

verbose = getOption("verbose"), acfLag0 = FALSE, ...)Arguments

- x

for 'acf': a numeric vector or time series.

for 'plot.acf': an object of class 'acf'.

- lag.max

maximum lag at which to calculate the acf.

- ci

coverage probability for confidence interval for 'plot.acf'.

- type

the type of 'acf' or 'plot'

- plot

logical. If 'TRUE' the 'acf' function will call 'plot.acf'.

- na.action

function to be called by 'acf' to handle missing values.

- demean

logical: Should the x be replaced by

x - mean(x)before computing the sums of squares and lagged cross products to produce the 'acf'?- xlab,ylab,ylim,main,ci.col,ci.type,max.mfrow,ask,mar,oma,mgp,xpd,cex.main,verbose

see the help page of

acf:help('acf', package = 'stats').- acfLag0

logical: TRUE to plot the traditional noninformation unit spike at lag 0. FALSE to omit that spike, consistent with the style in Tsay (2005).

- ...

further arguments passed to 'plot.acf'.

Details

These functions are provided to make it easy to plot an autocorrelation function without the noninformative unit spike at lag 0. This is done by calling plot(x, acfLag0 = FALSE, ...). Apart from the 'acfLag0' argument, the rest of the arguments are identical to those for 'acf' and 'plot.acf'.

Value

for acf, an object of class 'Acf', which inherits

from class 'acf', as described with help('acf', package='stats').

for plot.Acf, NULL

Examples

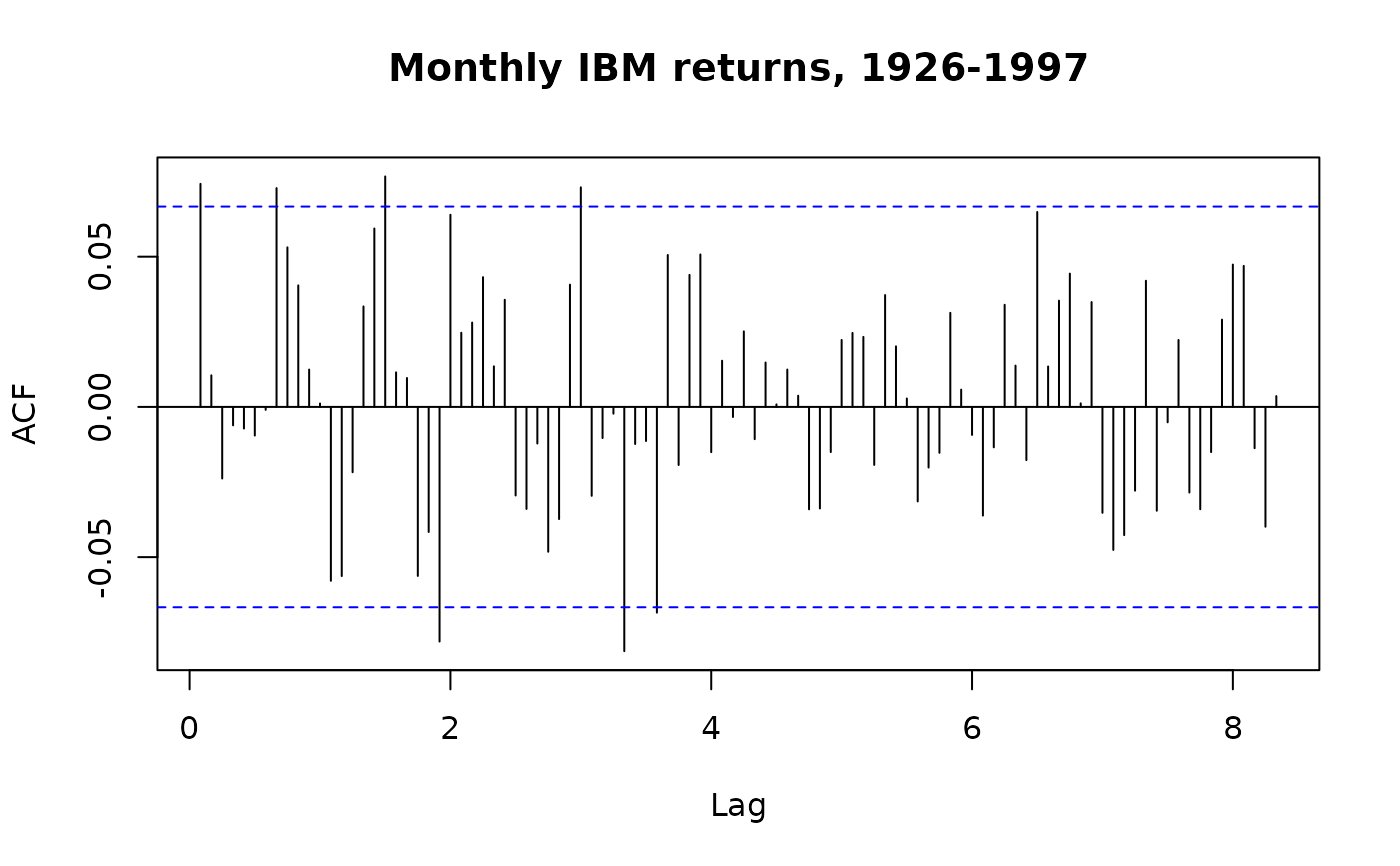

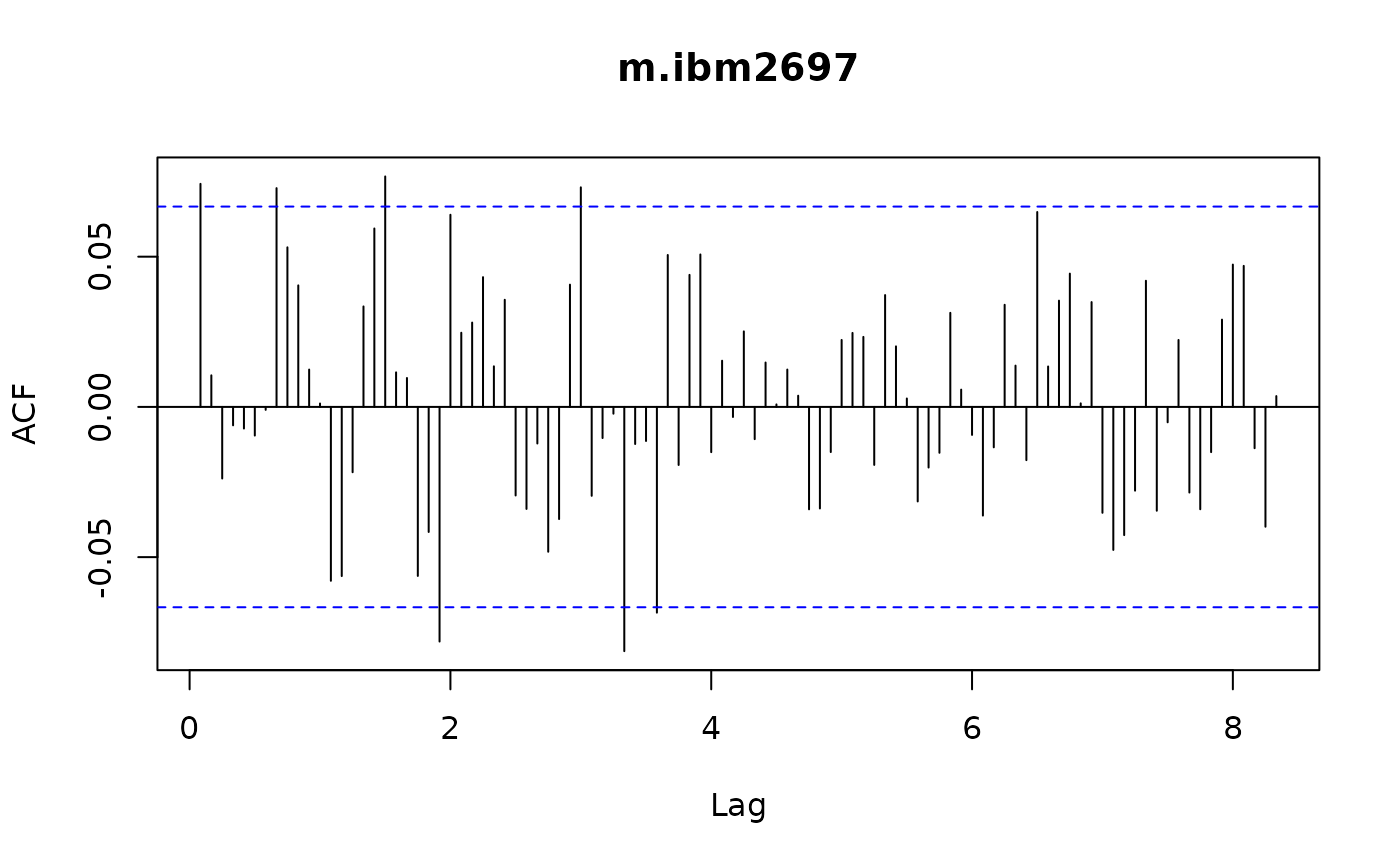

data(m.ibm2697)

Acf(m.ibm2697)

Acf(m.ibm2697, lag.max=100)

Acf(m.ibm2697, lag.max=100)

Acf(m.ibm2697, lag.max=100, main='Monthly IBM returns, 1926-1997')

Acf(m.ibm2697, lag.max=100, main='Monthly IBM returns, 1926-1997')