Fit normal, Student-t and stable distributions

dist-DistributionFits.RdA collection of moment and maximum likelihood estimators to fit the

parameters of a distribution.

The functions are:

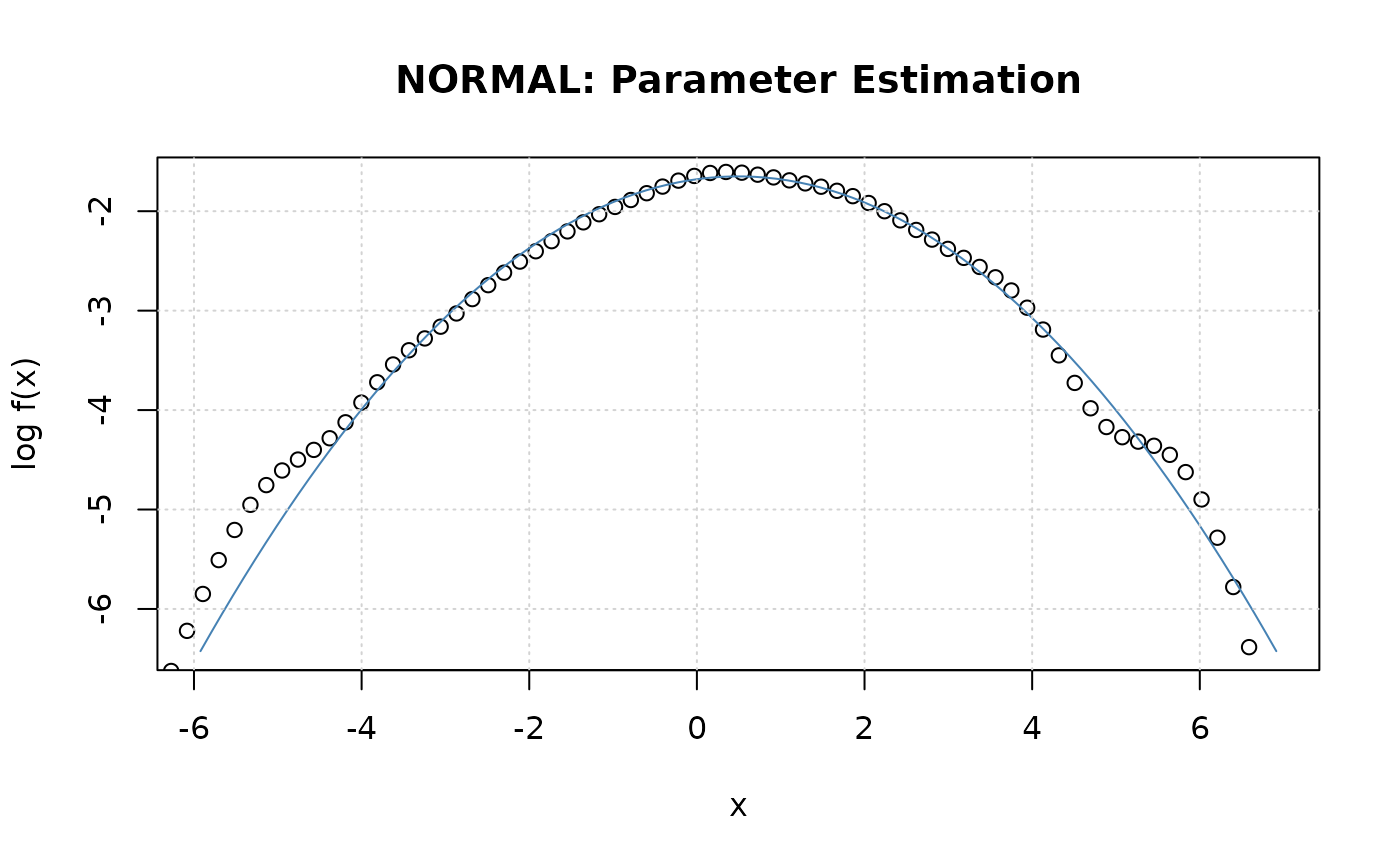

nFit | MLE parameter fit for a normal distribution, |

tFit | MLE parameter fit for a Student t-distribution, |

stableFit | MLE and Quantile Method stable parameter fit. |

Usage

nFit(x, doplot = TRUE, span = "auto", title = NULL, description = NULL, ...)

tFit(x, df = 4, doplot = TRUE, span = "auto", trace = FALSE, title = NULL,

description = NULL, ...)

stableFit(x, alpha = 1.75, beta = 0, gamma = 1, delta = 0,

type = c("q", "mle"), doplot = TRUE, control = list(),

trace = FALSE, title = NULL, description = NULL)Arguments

- x

a numeric vector.

- doplot

a logical flag. Should a plot be displayed?

- span

x-coordinates for the plot, by default 100 values automatically selected and ranging between the 0.001, and 0.999 quantiles. Alternatively, you can specify the range by an expression like

span=seq(min, max, times = n), where,minandmaxare the left and right endpoints of the range, andngives the number of the intermediate points.- control

a list of control parameters, see function

nlminb.- alpha, beta, gamma, delta

-

The parameters are

alpha,beta,gamma, anddelta:

value of the index parameteralphawithalpha = (0,2]; skewness parameterbeta, in the range [-1, 1]; scale parametergamma; and shift parameterdelta. - description

a character string which allows for a brief description.

- df

the number of degrees of freedom for the Student distribution,

df > 2, maybe non-integer. By default a value of 4 is assumed.- title

a character string which allows for a project title.

- trace

a logical flag. Should the parameter estimation process be traced?

- type

a character string which allows to select the method for parameter estimation:

"mle", the maximum log likelihood approach, or"qm", McCulloch's quantile method.- ...

parameters to be parsed.

Value

an object from class "fDISTFIT".

Slot fit has components estimate, minimum, code

and gradient (but for nFit code is NA and

gradient is missing).

Details

Stable Parameter Estimation:

Estimation techniques based on the quantiles of an empirical sample

were first suggested by Fama and Roll [1971]. However their technique

was limited to symmetric distributions and suffered from a small

asymptotic bias. McCulloch [1986] developed a technique that uses

five quantiles from a sample to estimate alpha and beta

without asymptotic bias. Unfortunately, the estimators provided by

McCulloch have restriction alpha>0.6.

Remark: The parameter estimation for the stable distribution via the maximum Log-Likelihood approach may take a quite long time.