Standardized generalized error distribution

dist-ged.RdFunctions to compute density, distribution function, quantile function and to generate random variates for the standardized generalized error distribution.

Usage

dged(x, mean = 0, sd = 1, nu = 2, log = FALSE)

pged(q, mean = 0, sd = 1, nu = 2)

qged(p, mean = 0, sd = 1, nu = 2)

rged(n, mean = 0, sd = 1, nu = 2)Details

The standardized GED is defined so that for a given sd it has

the same variance, sd^2, for all values of the shape parameter,

see the reference by Wuertz et al below.

dged computes the density,

pged the distribution function,

qged the quantile function,

and

rged generates random deviates from the standardized-t

distribution with the specified parameters.

References

Nelson D.B. (1991); Conditional Heteroscedasticity in Asset Returns: A New Approach, Econometrica, 59, 347–370.

Fernandez C., Steel M.F.J. (2000); On Bayesian Modelling of Fat Tails and Skewness, Preprint, 31 pages.

Wuertz D., Chalabi Y. and Luksan L. (????); Parameter estimation of ARMA models with GARCH/APARCH errors: An R and SPlus software implementation, Preprint, 41 pages, https://github.com/GeoBosh/fGarchDoc/blob/master/WurtzEtAlGarch.pdf

See also

gedFit,

absMoments,

sged (skew GED),

gedSlider for visualization

Examples

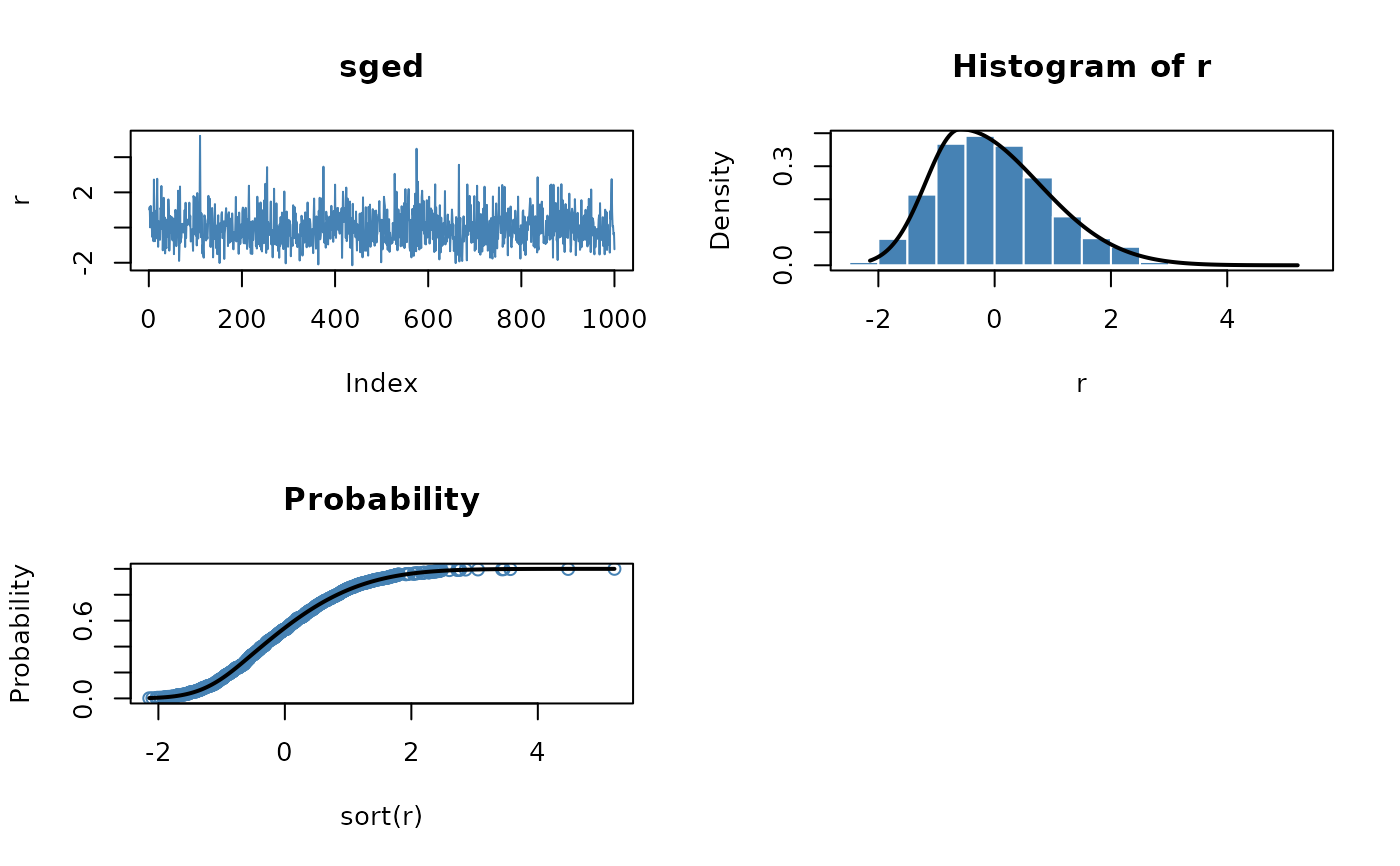

## sged -

par(mfrow = c(2, 2))

set.seed(1953)

r = rsged(n = 1000)

plot(r, type = "l", main = "sged", col = "steelblue")

# Plot empirical density and compare with true density:

hist(r, n = 25, probability = TRUE, border = "white", col = "steelblue")

box()

x = seq(min(r), max(r), length = 201)

lines(x, dsged(x), lwd = 2)

# Plot df and compare with true df:

plot(sort(r), (1:1000/1000), main = "Probability", col = "steelblue",

ylab = "Probability")

lines(x, psged(x), lwd = 2)

# Compute quantiles:

round(qsged(psged(q = seq(-1, 5, by = 1))), digits = 6)

#> [1] -1 0 1 2 3 4 5