Multi-step predictions for MixAR models

multiStep_dist-methods.RdMulti-step predictions for MixAR models.

Arguments

- model

a MixAR model.

- maxh

maximal horizon, a positive integer.

- N

an integer specifying the number of simulation samples to use, see 'Details. This argument is used only by simulation based methods.

- xcond

the past values needed for the conditional distribution, a numeric vector of length at least the maximal AR order of the components.

- ...

used only in some methods, see the details for the individual methods.

Details

The function currently implements two methods: the exact method due to Boshnakov (2009) and a simulation method described by (Wong and Li 2000) for Gaussian MixAR models but valid more generally.

The simulation method is available for any MixAR model, while the exact method is currently implemented only for models with Gaussian components ("MixARGaussian" class).

multiStep_dist returns a function which can be used to obtain

various properties of the predictive distribution for lags up to

maxh.

If argument N is missing the exact method is tried. Currently

an error will result if the exact method is not implemented for

model.

If argument N is given it must be a scalar numeric value, the

number of simulations to be performed to construct an approximation

for the predictive distributions.

The simulation is done by multiStep_dist. The properties

obtained later from the function returned by multiStep_dist use

the samples generated by the call to multiStep_dist.

To do a simulation with different parameters (e.g., with larger

N) call multiStep_dist again.

Details on the returned function

If xcond is missing multiStep_dist returns a function

with arguments h, what and xcond.

If xcond is supplied, then it is fixed to that value and the

arguments of the returned function are h, what and

'...'. The dots argument is currently used in the case of the

simulation method, see below.

Let f be the function returned by multiStep_dist.

Argument h is the required prediction horizon and can be a

number in the interval \([1,maxh]\). Argument what is the

required property of the predictive distribution for lag

h. If what is a function, it is applied to the simulated

sample for the requested horizon (currently available only for

the simulation method). If what is a character string, the

corresponding property of the predictive distribution for horizon

h is returned.

Currently possible values for what are:

- "pdf"

the probability density function.

- "cdf"

the cumulative distribution function.

- "location"

the location (conditional mean).

- "variance"

the conditional variance, a.k.a (squared) volatility.

- "sd"

the conditional standard deviation, a.k.a volatility.

- "skewness"

the conditional skewness.

- "kurtosis"

the conditional kurtosis.

Note that what = "pdf" and what = "cdf" return functions

even in the simulation case. For "pdf" the function is constructed

using density and the "..." arguments passed to f will

be passed on to density if finer control is needed.

If what is none of the above, the raw object is returned

currently (but this may change).

Methods

The Details section gives a rather detailed description of the function, so the descriptions below are brief.

signature(model = "MixAR", maxh = "numeric", N = "numeric", xcond = "numeric")Non-missing

Nrequests the simulation method. The predictive distribution is approximated by simulatingNof future paths up to horizonmaxhand using a non-parametric estimate. Arguments"..."are passed todensityto allow finer control.signature(model = "MixARGaussian", maxh = "numeric", N = "missing", xcond = "missing")Computes the predictive distribution using the exact method. Returns a function with arguments

h,whatandxcond.signature(model = "MixARGaussian", maxh = "numeric", N = "missing", xcond = "ANY")Computes the predictive distribution using the exact method. Returns a function with arguments

handwhat. (i.e.,xcondis fixed to the supplied argumentxcond).

References

Boshnakov GN (2009).

“Analytic expressions for predictive distributions in mixture autoregressive models.”

Stat. Probab. Lett., 79(15), 1704-1709.

doi:10.1016/j.spl.2009.04.009

.

Wong CS, Li WK (2000).

“On a mixture autoregressive model.”

J. R. Stat. Soc., Ser. B, Stat. Methodol., 62(1), 95-115.

Examples

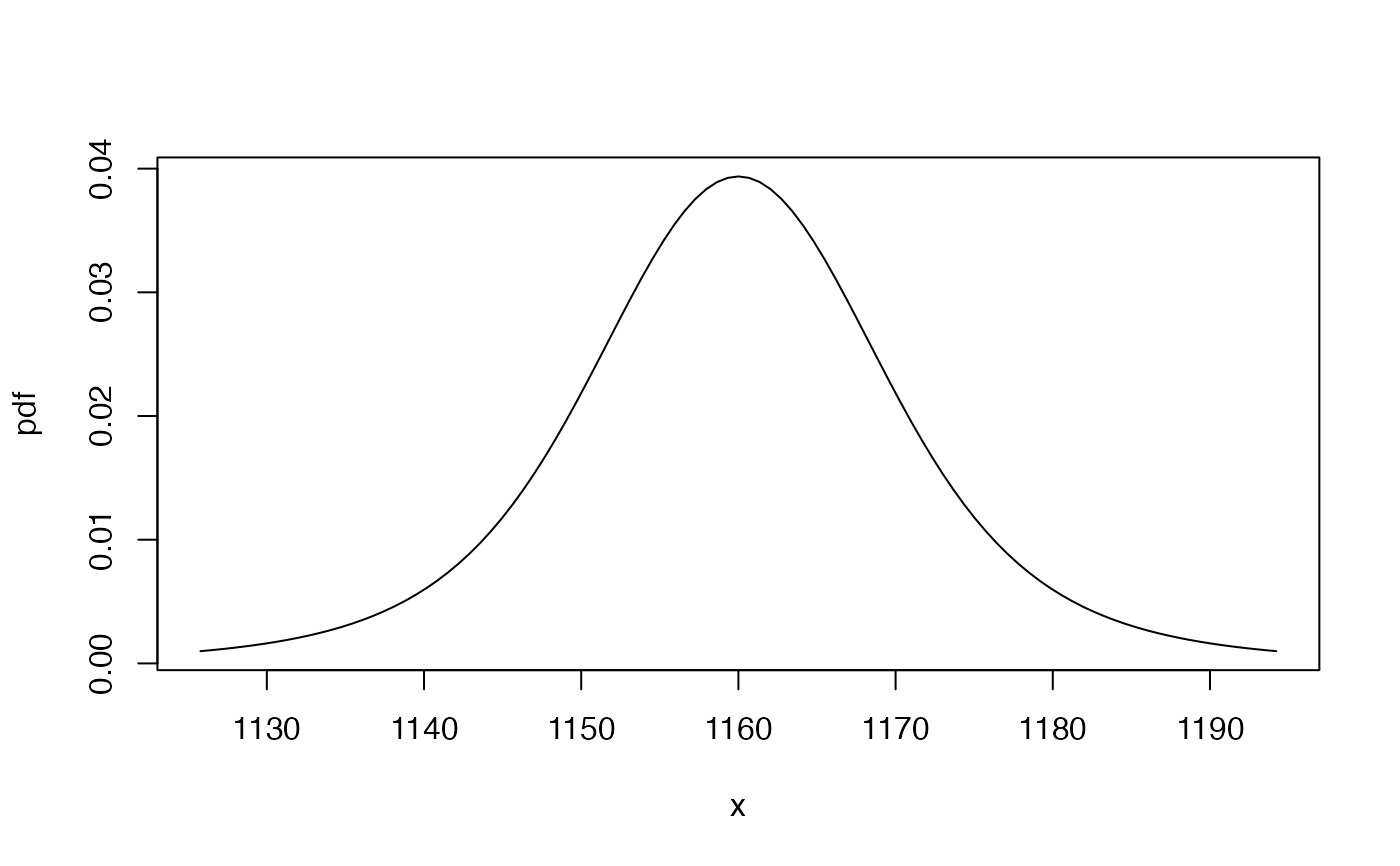

## exact method, without xcond

dist <- multiStep_dist(exampleModels$WL_ibm, maxh = 3)

tfpdf <- dist(3, "pdf", xcond = c(560, 600)) # xcond is argument to 'dist' here

tfcdf <- dist(3, "cdf", xcond = c(560, 600))

## plot the pdf (gbutils::plotpdf determines suitable range automatically)

gbutils::plotpdf(tfpdf, cdf = tfcdf)

args(dist(3, "pdf", xcond = c(500, 600))) # x

#> function (x)

#> NULL

## use a simulation method with N = 1000

tf <- multiStep_dist(exampleModels$WL_ibm, maxh = 3, N = 1000, xcond = c(560, 600))

args(tf) # (h, what, ...)

#> function (h, what, ...)

#> NULL

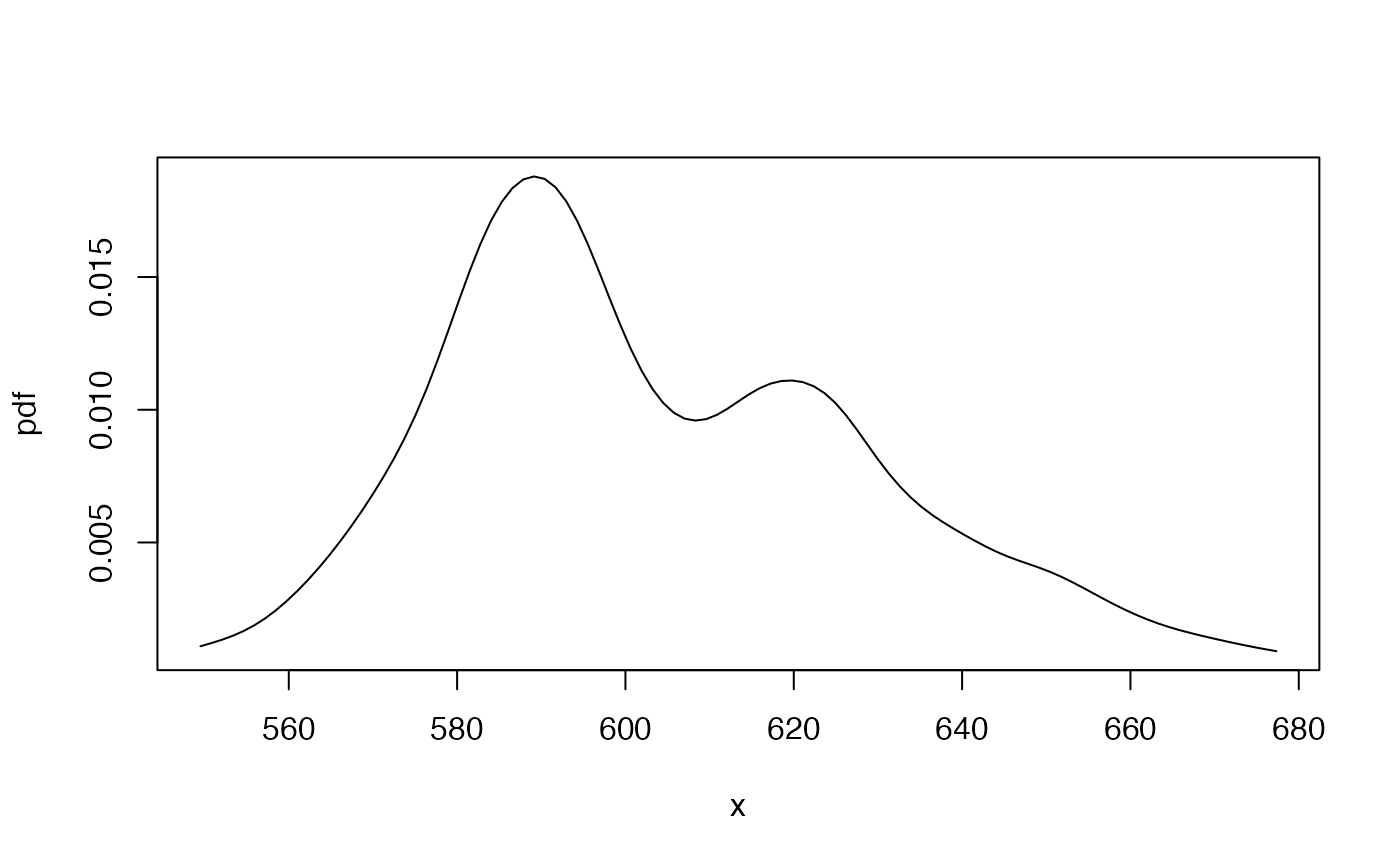

## the exact method may also be used with fixed xcond:

tfe <- multiStep_dist(exampleModels$WL_ibm, maxh = 3, xcond = c(560, 600))

## get pdf and cdf for horizon 3

tfepdf <- tfe(3, "pdf")

tfecdf <- tfe(3, "cdf")

## plot the pdf

gbutils::plotpdf(tfepdf, cdf = tfecdf)

tf(3, "location")

#> [1] 604.3241

tf(1, "location")

#> [1] 604.7039

mix_location(exampleModels$WL_ibm, xcond = c(560, 600))

#> [1] 604.2307

## larger simulation gives better approximation, in general

tf <- multiStep_dist(exampleModels$WL_ibm, maxh = 3, N = 10000, xcond = c(560, 600))

tf(1, "location")

#> [1] 604.1066

tf1000pdf <- tf(3, "pdf")

tf1000cdf <- tf(3, "cdf")

gbutils::plotpdf(tf1000pdf, cdf = tf1000cdf)

args(dist(3, "pdf", xcond = c(500, 600))) # x

#> function (x)

#> NULL

## use a simulation method with N = 1000

tf <- multiStep_dist(exampleModels$WL_ibm, maxh = 3, N = 1000, xcond = c(560, 600))

args(tf) # (h, what, ...)

#> function (h, what, ...)

#> NULL

## the exact method may also be used with fixed xcond:

tfe <- multiStep_dist(exampleModels$WL_ibm, maxh = 3, xcond = c(560, 600))

## get pdf and cdf for horizon 3

tfepdf <- tfe(3, "pdf")

tfecdf <- tfe(3, "cdf")

## plot the pdf

gbutils::plotpdf(tfepdf, cdf = tfecdf)

tf(3, "location")

#> [1] 604.3241

tf(1, "location")

#> [1] 604.7039

mix_location(exampleModels$WL_ibm, xcond = c(560, 600))

#> [1] 604.2307

## larger simulation gives better approximation, in general

tf <- multiStep_dist(exampleModels$WL_ibm, maxh = 3, N = 10000, xcond = c(560, 600))

tf(1, "location")

#> [1] 604.1066

tf1000pdf <- tf(3, "pdf")

tf1000cdf <- tf(3, "cdf")

gbutils::plotpdf(tf1000pdf, cdf = tf1000cdf)

## plot the exact and simulated pdf's together for comparison

gbutils::plotpdf(tfepdf, cdf = tfecdf)

curve(tf1000pdf, add = TRUE, col = "red")

## plot the exact and simulated pdf's together for comparison

gbutils::plotpdf(tfepdf, cdf = tfecdf)

curve(tf1000pdf, add = TRUE, col = "red")

## get the raw data

tfs <- tf(1, "sampled")

apply(tfs, 2, mean) # location for lags from 1 to maxh (here 3)

#> [1] 604.1066 604.7578 604.8559

tf(1, "location")

#> [1] 604.1066

tf(1, "variance")

#> [1] 415.2029

tf(1, "sd")

#> [1] 20.37653

mix_variance(exampleModels$WL_ibm, xcond = c(560, 600))

#> [1] 413.0203

sqrt(mix_variance(exampleModels$WL_ibm, xcond = c(560, 600)))

#> [1] 20.3229

mix_kurtosis(exampleModels$WL_ibm, xcond = c(359, 200))

#> [1] 1.135385

mix_kurtosis(exampleModels$WL_ibm, xcond = c(359, 400))

#> [1] 1.392797

## get the raw data

tfs <- tf(1, "sampled")

apply(tfs, 2, mean) # location for lags from 1 to maxh (here 3)

#> [1] 604.1066 604.7578 604.8559

tf(1, "location")

#> [1] 604.1066

tf(1, "variance")

#> [1] 415.2029

tf(1, "sd")

#> [1] 20.37653

mix_variance(exampleModels$WL_ibm, xcond = c(560, 600))

#> [1] 413.0203

sqrt(mix_variance(exampleModels$WL_ibm, xcond = c(560, 600)))

#> [1] 20.3229

mix_kurtosis(exampleModels$WL_ibm, xcond = c(359, 200))

#> [1] 1.135385

mix_kurtosis(exampleModels$WL_ibm, xcond = c(359, 400))

#> [1] 1.392797