Tests for weak white noise

acfGarchTest.RdCarry out tests for weak white noise under GARCH, GARCH-type, and stochastic volatility null hypotheses.

Arguments

- acr

autocorrelations.

- x

time series.

- nlags

how many lags to use.

- interval

If not NULL, compute also confidence intervals with the specified coverage probability.

- ...

additional arguments for the computation of the variance matrix under the null hypothesis, passed on to

nvarOfAcfKP.

Details

Unlike the autocorrelation IID test, the time series is needed here to estimate the covariance matrix of the autocorrelations under the null hypothesis.

acfGarchTest performs a test for uncorrelatedness of a time

series. The null hypothesis is that the time series is GARCH,

see Francq and Zakoian (2010)

.

acfWnTest performs a test for uncorrelatedness of a time

series under a weaker null hypothesis.

The null hypothesis is that the time series is GARCH-type or

from a stochasitc volatily model,

see Kokoszka and Politis (2011)

.

See the references for details and precise specification of the hypotheses.

The format of the return value is the same as for acfIidTest.

References

Francq C, Zakoian J (2010).

GARCH models: structure, statistical inference and financial applications.

John Wiley & Sons.

ISBN 978-0-470-68391-0.

Kokoszka PS, Politis DN (2011).

“Nonlinearity of ARCH and stochastic volatility models and Bartlett's formula.”

Probability and Mathematical Statistics, 31(1), 47--59.

See also

plot-methods for graphical representations of results

Examples

## see also the examples for \code{\link{whiteNoiseTest}}

set.seed(1234)

n <- 5000

x <- sarima:::rgarch1p1(n, alpha = 0.3, beta = 0.55, omega = 1, n.skip = 100)

x.acf <- autocorrelations(x)

x.pacf <- partialAutocorrelations(x)

acfGarchTest(x.acf, x = x, nlags = c(5,10,20))

#> $test

#> h Q pval

#> [1,] 5 2.867048 0.7204741

#> [2,] 10 9.064633 0.5259808

#> [3,] 20 24.420187 0.2245192

#>

#> $ci

#> int

#> [1,] -0.05923087 0.05923087

#> [2,] -0.05326386 0.05326386

#> [3,] -0.05066191 0.05066191

#> [4,] -0.04522221 0.04522221

#> [5,] -0.04507543 0.04507543

#> [6,] -0.04189048 0.04189048

#> [7,] -0.04210249 0.04210249

#> [8,] -0.03890700 0.03890700

#> [9,] -0.03517673 0.03517673

#> [10,] -0.03572033 0.03572033

#> [11,] -0.03155470 0.03155470

#> [12,] -0.03222239 0.03222239

#> [13,] -0.03105026 0.03105026

#> [14,] -0.03010171 0.03010171

#> [15,] -0.02875639 0.02875639

#> [16,] -0.02686352 0.02686352

#> [17,] -0.02775162 0.02775162

#> [18,] -0.02700132 0.02700132

#> [19,] -0.02673210 0.02673210

#> [20,] -0.02709457 0.02709457

#>

acfGarchTest(x.pacf, x = x, nlags = c(5,10,20))

#> $test

#> h Q pval

#> [1,] 5 2.884453 0.7177943

#> [2,] 10 9.183271 0.5148034

#> [3,] 20 27.271537 0.1277959

#>

#> $ci

#> int

#> [1,] -0.05923087 0.05923087

#> [2,] -0.05326386 0.05326386

#> [3,] -0.05066191 0.05066191

#> [4,] -0.04522221 0.04522221

#> [5,] -0.04507543 0.04507543

#> [6,] -0.04189048 0.04189048

#> [7,] -0.04210249 0.04210249

#> [8,] -0.03890700 0.03890700

#> [9,] -0.03517673 0.03517673

#> [10,] -0.03572033 0.03572033

#> [11,] -0.03155470 0.03155470

#> [12,] -0.03222239 0.03222239

#> [13,] -0.03105026 0.03105026

#> [14,] -0.03010171 0.03010171

#> [15,] -0.02875639 0.02875639

#> [16,] -0.02686352 0.02686352

#> [17,] -0.02775162 0.02775162

#> [18,] -0.02700132 0.02700132

#> [19,] -0.02673210 0.02673210

#> [20,] -0.02709457 0.02709457

#>

# do not compute CI's:

acfGarchTest(x.pacf, x = x, nlags = c(5,10,20), interval = NULL)

#> $test

#> h Q pval

#> [1,] 5 2.884453 0.7177943

#> [2,] 10 9.183271 0.5148034

#> [3,] 20 27.271537 0.1277959

#>

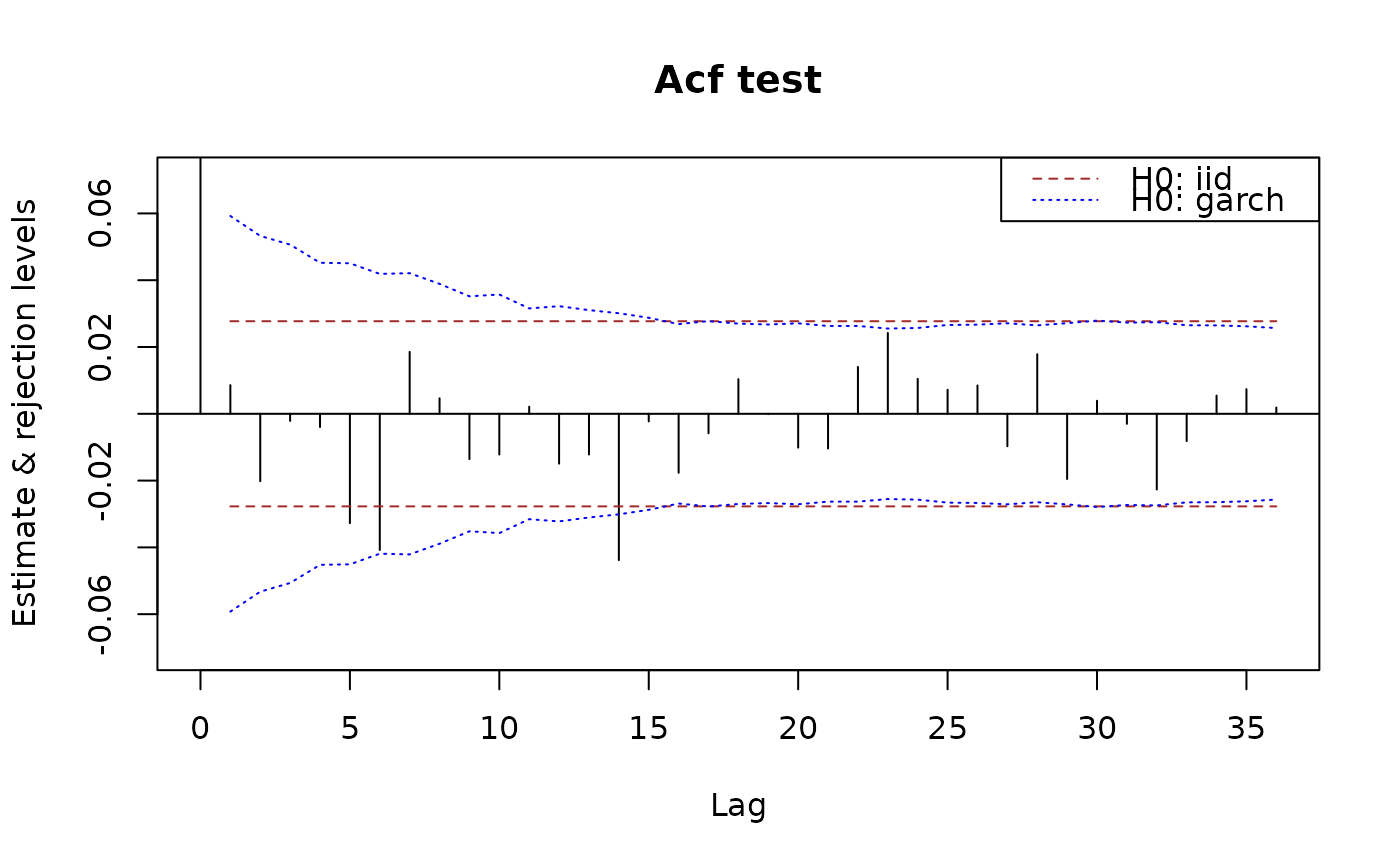

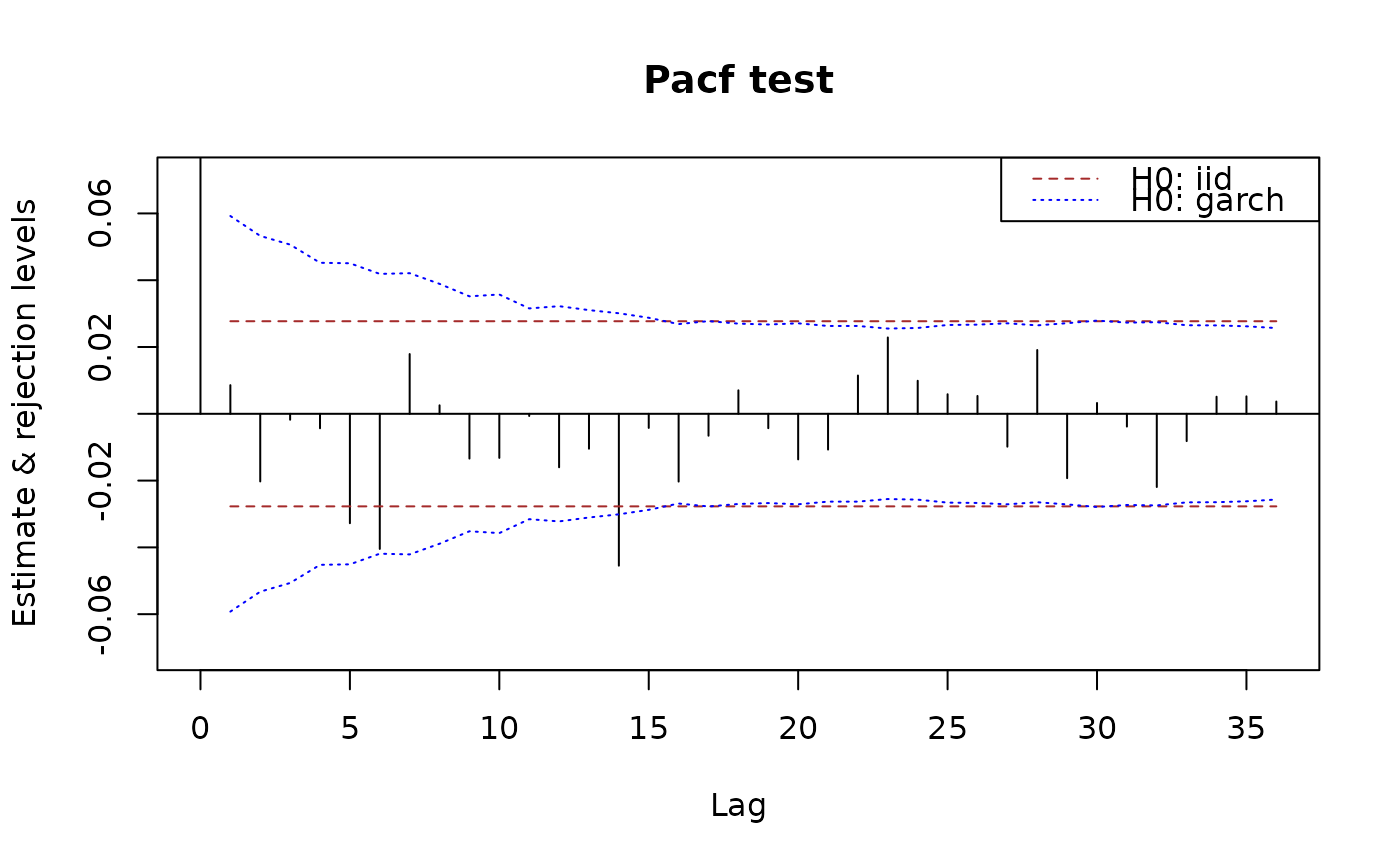

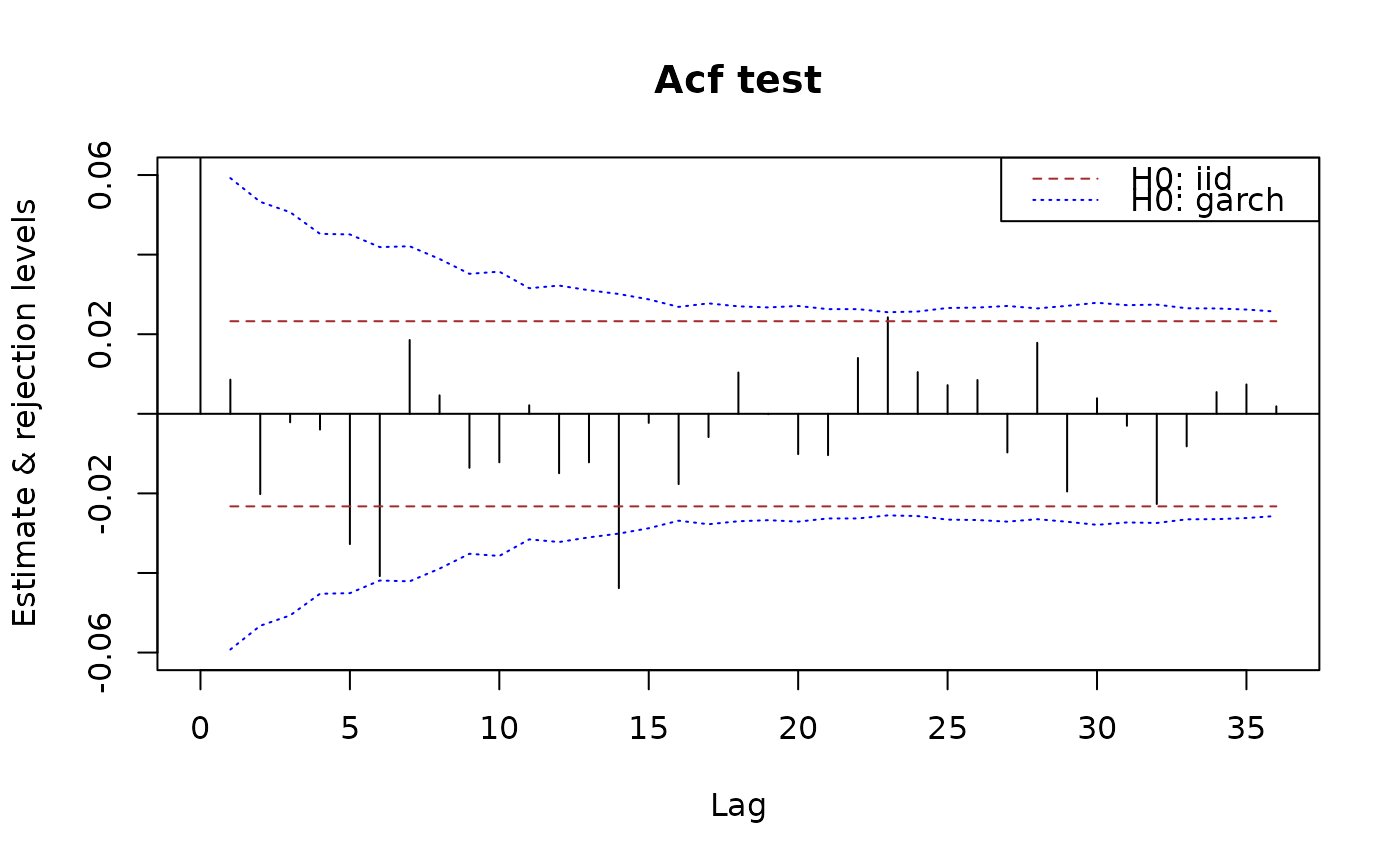

## plot methods call acfGarchTest() suitably if 'x' is given:

plot(x.acf, data = x)

plot(x.pacf, data = x)

plot(x.pacf, data = x)

## use 90% limits:

plot(x.acf, data = x, interval = 0.90)

## use 90% limits:

plot(x.acf, data = x, interval = 0.90)

acfWnTest(x.acf, x = x, nlags = c(5,10,20))

#> $test

#> h Q pval

#> [1,] 5 2.695352 0.7468293

#> [2,] 10 8.157398 0.6134657

#> [3,] 20 20.691112 0.4155097

#>

#> $ci

#> int

#> [1,] -0.05923087 0.05923087

#> [2,] -0.05326386 0.05326386

#> [3,] -0.05066191 0.05066191

#> [4,] -0.04522221 0.04522221

#> [5,] -0.04507543 0.04507543

#> [6,] -0.04189048 0.04189048

#> [7,] -0.04210249 0.04210249

#> [8,] -0.03890700 0.03890700

#> [9,] -0.03517673 0.03517673

#> [10,] -0.03572033 0.03572033

#> [11,] -0.03155470 0.03155470

#> [12,] -0.03222239 0.03222239

#> [13,] -0.03105026 0.03105026

#> [14,] -0.03010171 0.03010171

#> [15,] -0.02875639 0.02875639

#> [16,] -0.02686352 0.02686352

#> [17,] -0.02775162 0.02775162

#> [18,] -0.02700132 0.02700132

#> [19,] -0.02673210 0.02673210

#> [20,] -0.02709457 0.02709457

#>

nvarOfAcfKP(x, maxlag = 20)

#> [1] 4.5663595 3.6926586 3.3406961 2.6618118 2.6445613 2.2840442 2.3072224

#> [8] 1.9702857 1.6105891 1.6607521 1.2959906 1.3514172 1.2548862 1.1793864

#> [15] 1.0763228 0.9392902 1.0024221 0.9489510 0.9301220 0.9555168

whiteNoiseTest(x.acf, h0 = "arch-type", x = x, nlags = c(5,10,20))

#> $test

#> h Q pval

#> [1,] 5 2.695352 0.7468293

#> [2,] 10 8.157398 0.6134657

#> [3,] 20 20.691112 0.4155097

#>

#> $ci

#> int

#> [1,] -0.05923087 0.05923087

#> [2,] -0.05326386 0.05326386

#> [3,] -0.05066191 0.05066191

#> [4,] -0.04522221 0.04522221

#> [5,] -0.04507543 0.04507543

#> [6,] -0.04189048 0.04189048

#> [7,] -0.04210249 0.04210249

#> [8,] -0.03890700 0.03890700

#> [9,] -0.03517673 0.03517673

#> [10,] -0.03572033 0.03572033

#> [11,] -0.03155470 0.03155470

#> [12,] -0.03222239 0.03222239

#> [13,] -0.03105026 0.03105026

#> [14,] -0.03010171 0.03010171

#> [15,] -0.02875639 0.02875639

#> [16,] -0.02686352 0.02686352

#> [17,] -0.02775162 0.02775162

#> [18,] -0.02700132 0.02700132

#> [19,] -0.02673210 0.02673210

#> [20,] -0.02709457 0.02709457

#>

acfWnTest(x.acf, x = x, nlags = c(5,10,20))

#> $test

#> h Q pval

#> [1,] 5 2.695352 0.7468293

#> [2,] 10 8.157398 0.6134657

#> [3,] 20 20.691112 0.4155097

#>

#> $ci

#> int

#> [1,] -0.05923087 0.05923087

#> [2,] -0.05326386 0.05326386

#> [3,] -0.05066191 0.05066191

#> [4,] -0.04522221 0.04522221

#> [5,] -0.04507543 0.04507543

#> [6,] -0.04189048 0.04189048

#> [7,] -0.04210249 0.04210249

#> [8,] -0.03890700 0.03890700

#> [9,] -0.03517673 0.03517673

#> [10,] -0.03572033 0.03572033

#> [11,] -0.03155470 0.03155470

#> [12,] -0.03222239 0.03222239

#> [13,] -0.03105026 0.03105026

#> [14,] -0.03010171 0.03010171

#> [15,] -0.02875639 0.02875639

#> [16,] -0.02686352 0.02686352

#> [17,] -0.02775162 0.02775162

#> [18,] -0.02700132 0.02700132

#> [19,] -0.02673210 0.02673210

#> [20,] -0.02709457 0.02709457

#>

nvarOfAcfKP(x, maxlag = 20)

#> [1] 4.5663595 3.6926586 3.3406961 2.6618118 2.6445613 2.2840442 2.3072224

#> [8] 1.9702857 1.6105891 1.6607521 1.2959906 1.3514172 1.2548862 1.1793864

#> [15] 1.0763228 0.9392902 1.0024221 0.9489510 0.9301220 0.9555168

whiteNoiseTest(x.acf, h0 = "arch-type", x = x, nlags = c(5,10,20))

#> $test

#> h Q pval

#> [1,] 5 2.695352 0.7468293

#> [2,] 10 8.157398 0.6134657

#> [3,] 20 20.691112 0.4155097

#>

#> $ci

#> int

#> [1,] -0.05923087 0.05923087

#> [2,] -0.05326386 0.05326386

#> [3,] -0.05066191 0.05066191

#> [4,] -0.04522221 0.04522221

#> [5,] -0.04507543 0.04507543

#> [6,] -0.04189048 0.04189048

#> [7,] -0.04210249 0.04210249

#> [8,] -0.03890700 0.03890700

#> [9,] -0.03517673 0.03517673

#> [10,] -0.03572033 0.03572033

#> [11,] -0.03155470 0.03155470

#> [12,] -0.03222239 0.03222239

#> [13,] -0.03105026 0.03105026

#> [14,] -0.03010171 0.03010171

#> [15,] -0.02875639 0.02875639

#> [16,] -0.02686352 0.02686352

#> [17,] -0.02775162 0.02775162

#> [18,] -0.02700132 0.02700132

#> [19,] -0.02673210 0.02673210

#> [20,] -0.02709457 0.02709457

#>